Your Privacy Choices

Your Privacy Choices

Good morning quiet shooters and welcome back to another edition of TFB’s Silencer Saturday brought to you by Yankee Hill Machine, manufacturers of the YHM Nitro N20 suppressor. Last week we discussed a unique subsonic ammunition solution from Seismic Ammo – 185gr bullets in a 9mm cartridge traveling at about 1000fps. This week we look at the regulatory side of NFA 2020. Are we making forward progress in 2020?

SILENCER SATURDAY #129: NFA 2020 – Rights Still Delayed; Rights Still Denied

We obviously don’t do the whole bipartisan politics, sensationalist journalism shtick here at TFB, but we still have to be able to discuss laws, regulations and other government intervention that prevents the free expression of individual liberty. For me, the biggest example of these rights denied to American gun owners is the National Firearms Act of 1934. Specifically, silencers that are just highly engineered mufflers incapable of shooting a bullet on their own, were taxed into oblivion – approximately $4,000 in today’s money would mean that nearly everyone, except to the ultra wealthy, would be prevented from owning silencers.

Luckily for us, the $200 tax hasn’t increased with inflation in the last ~85 years, making them financially obtainable. On the flip side, we’ve gone from a few days for an application approval to nine months to a year average. All for a device that should be sold over the counter like brakes and flash hiders.

SILENCER SATURDAY #129: NFA 2020 – Rights Still Delayed; Rights Still Denied – Oldest Form 1?

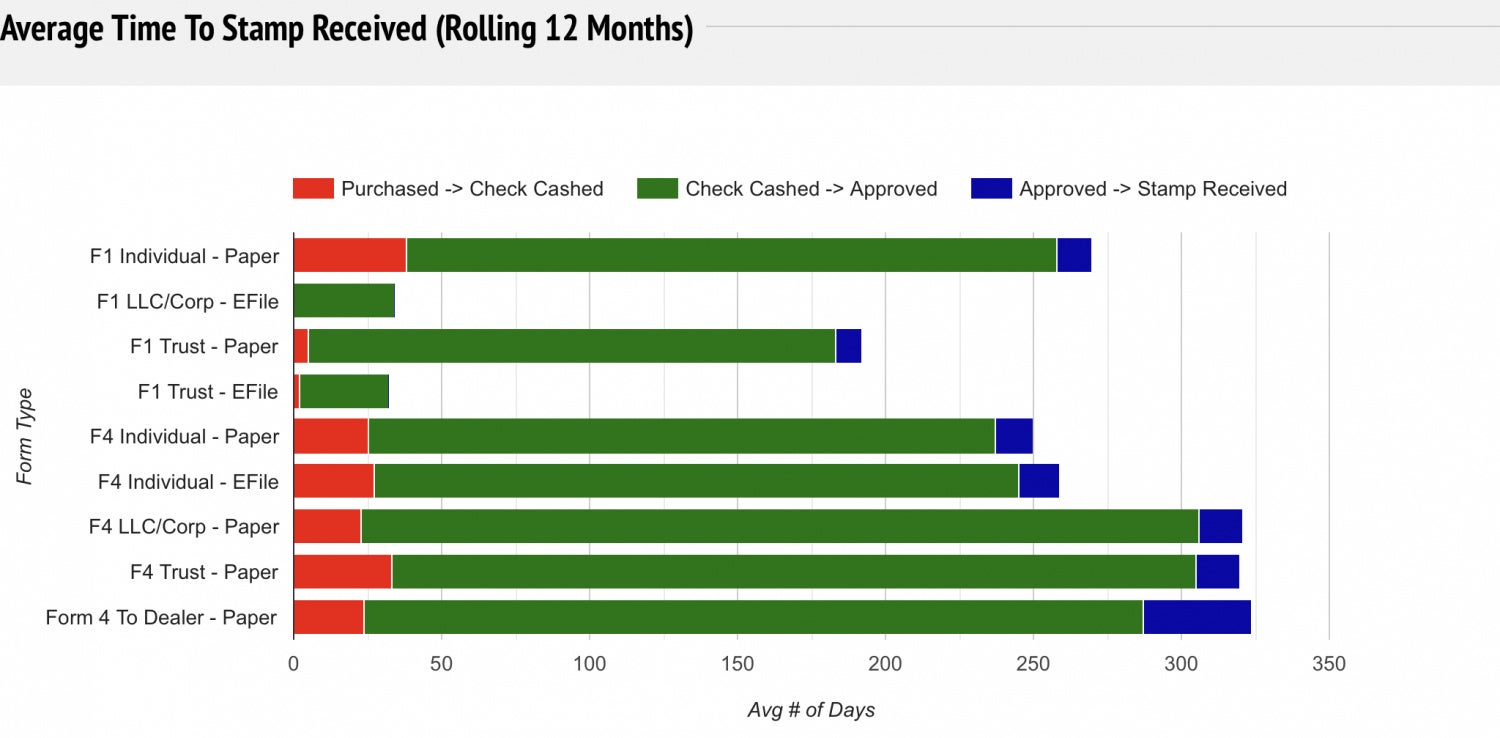

NFA Transfer Times – June 2020

NFA Tracker: https://www.nfatracker.com

While Form 1 (making) applications using the ATF eForm system are averaging two-week approvals, Form 4 (transfer) application approvals, on the other hand, still take as much time as it does to find a mate, conceive, gestate and birth a new human being. It’s shocking really when you think about it.

There is still no update for the return of eForm Form 4 applications and I’d guess that Covid will be blamed for the lack of funding or resources to keep the late 2020/early 2021 estimated timetable. Absent the abolition of the NFA, the return of eForm Form 4 applications will have the biggest impact on the current system.

Speaking of which, we are almost ready to embark upon the second phase of our Form 1 journey in the Build Your Own Suppressor series here at TFB. My approval came back in about 12 days, including weekends.

SILENCER SATURDAY #129: NFA 2020 – Rights Still Delayed; Rights Still Denied

SILENCER SATURDAY #129: NFA 2020 – Rights Still Delayed; Rights Still Denied – Form 1 Suppressor

H.R.6126 – End the Normalized Delay of Suppressors Act of 2020

In an attempt to cap the approval wait times for suppressors, there is a proposed bill in the House to cap approval times to a maximum wait of 90 days. In the event that the application is not approved in 90 days, the silencer can be transferred to the individual or entity.

I’d love for H6 6126to gain traction, but I have very little hope it will ever see any movement at all.

To amend the Internal Revenue Code of 1986 to allow the transfer of a silencer after the end of the 90-day period beginning with the application for such transfer.

Congress.gov: https://www.congress.gov/bill/116th-congress/house-bill/6126/text

SEC. 2. 90-DAY APPLICATION PERIOD FOR TRANSFER OF SILENCERS.

(a) In General.--Section 5812 of the Internal Revenue Code of 1986

is amended by adding at the end the following new subsection:

``(c) 90-Day Application Period for Silencers.--In the case of a

transfer of a silencer, such transfer may be made, notwithstanding

subsection (a), if 90 days have elapsed since the application required

by such subsection was filed with respect to such silencer, and such

application has not been denied.''.

(b) Effective Date.--The amendments made by this section shall

apply to transfers more than 180 days after the date of the enactment

of this Act.

Speaking of support, the ASA has a new membership drive contest and raffle coming up. Keep an eye out starting this week .

News: Panel Asked to Toss Gun Conviction of Accused Shooting Plotter

This is an interesting take on the constitutionality of taxation when it comes to NFA regulations in the appeal process of a criminal conviction. Representing a client who was arrested for buying an unregistered silencer through an undercover deal with a detective, the attorney argues that the NFA tax should be paid by either the maker or the transferor, not the transferee.

During Thursday’s oral arguments before the 11th Circuit, held via teleconference due to the Covid-19 pandemic, public defender Lynn Bailey made her case on why Bolatete’s conviction exceeds Congress’s power to tax and violates the Second Amendment by requiring him to pay for a constitutionally protected right.

Bailey questioned why Bolatete, the buyer of the unregistered silencer, had a duty to register the device and purchase the tax stamp, and not the seller – in this case, the undercover detective.

“It makes more sense to me for the maker or transferor” to pay the tax, Bailey told the three-judge panel of the Atlanta-based appeals court. “They are the ones responsible for paying the tax … But here you are punishing the transferee with 10 years in prison ostensibly for a tax that someone else is required to pay, and he doesn’t know whether it’s paid or not.”

U.S. Circuit Judge Ed Carnes interjected.

“We get taxed all the time by things we don’t know during transactions,” the Ronald Reagan appointee said. “But nobody’s ever suggested that means it’s an invalid exercise of the taxing power.”

He also noted the person receiving the firearm “could determine whether the tax was paid or not by asking the transferor, couldn’t he?”

Bailey argued the responsibility should not lie on the buyer.

“What we’re really arguing here is the punishment of the downstream possessor, this downstream transferee, does not aid with any revenue purpose,” she said. “This is a punitive statute and not a taxing statute … There is something offensive about incentivizing imprisoning the transferee and shifting the burden of knowledge, the burden to inquire about the tax stamp, to the transferee.”

I wish I had better news for you all – even without Covid-19 and civil unrest, 2020 was always going to be a difficult year to make any forward progress. Both sides of the political system are drawing hard lines in the sand and hunkering down. I can’t imagine any meaningful legislation to occur before the end of the end of the year, let alone for something firearms related.

Have a great week. Thanks for your support and see you here at TFB for another edition of Silencer Saturday.

Silencer Saturday is Sponsored by Yankee Hill Machine:

Buy YHM silencers and accessories at:

Silencer Shop – Hansohn BrOthers – dead eye gun supply –

Mac tactical

All YHM Products At Brownells

DEALERS: If you want your link to buy YHM suppressors included in future Silencer Saturday posts, email: silencers@thefirearmblog.com